Tally your AMT rate with an alternative minimum tax calculator

Taxes are confusing. They come with forms, rules, exceptions to the rules, and sometimes even penalties for not understanding the rules.

But if there’s one tax that consistently baffles people, especially high earners, it’s the Alternative Minimum Tax (AMT).

The number of AMT payers is expected to be around 7.6 million people in 2026. This follows the expiration of the Tax Cuts and Jobs Act (TCJA) by the end of 2025, which lessened the impact of the AMT.

So if you’re surprised with a bigger tax bill than you expected in the future, the AMT might be why. Fortunately, you can use an AMT tax calculator to estimate your liability before tax season sneaks up on you.

Let’s break it down:

What is the alternative minimum tax (AMT)?

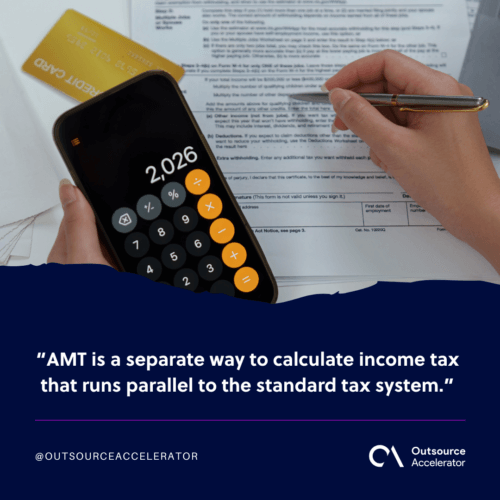

AMT is a separate way to calculate income tax that runs parallel to the standard tax system. It removes many deductions and adds back income items that the regular system doesn’t count.

If the amount you owe under the AMT calculation is higher than what you’d pay normally, you have to pay the higher amount.

The AMT was introduced in 1969 after news broke that 155 high-income households paid zero federal income tax. The idea was simple: Prevent wealthy individuals from avoiding taxes through deductions and loopholes.

Today, the AMT applies mostly to upper-middle-class and high-income taxpayers: those earning between $200,000 and $1 million annually, depending on filing status and deductions.

The IRS uses a separate set of rules to determine taxable income under the AMT. Common deductions, such as state and local taxes, personal exemptions, and miscellaneous itemized deductions, don’t apply.

This means your taxable income under AMT rules could be significantly higher than under regular tax rules.

Who needs to pay for the AMT?

The AMT mostly affects individuals and families with higher incomes, especially those who claim large deductions or have incentive stock options.

You might be subject to the alternative minimum tax if:

- You earn more than $200,000 per year

- You claim high deductions for state and local taxes (SALT)

- You have significant income from capital gains or incentive stock options

- You deduct mortgage interest on home equity loans not used to buy, build, or improve your home

- You claim multiple dependents or other itemized deductions

Even if you don’t meet all these criteria, it’s smart to check. AMT thresholds adjust annually with inflation, and the AMT exemption begins to phase out at $609,350 for single filers and $1,218,700 for married couples filing jointly (for 2024).

How to compute and pay with an AMT tax calculator

Using an AMT tax calculator is the easiest way to estimate whether you owe the AMT. You can find these tools on tax software websites or financial planning platforms.

While each calculator varies slightly, most will walk you through inputs like income, deductions, filing status, and credits.

Here’s a simplified step-by-step:

1. Calculate your alternative minimum taxable income (AMTI)

Start with your gross income, then add back deductions that aren’t allowed under the AMT. These could include SALT deductions, personal exemptions, or miscellaneous deductions.

2. Subtract the AMT exemption amount

For 2024, the exemption is $85,700 for single filers and $133,300 for joint filers. This amount phases out for higher earners.

3. Apply the AMT tax rates

The AMT uses two rates: 26% and 28%. Income up to $232,600 (for 2024) is taxed at 26%. Anything above that is taxed at 28%.

4. Compare with your regular tax

If your AMT is higher, you owe the difference.

5. File using IRS Form 6251

This IRS form calculates the AMT and determines whether it applies to your return. It’s attached to your regular Form 1040 when filing.

Is it possible to avoid having an AMT?

There’s no magic way to eliminate the AMT, but you can reduce the chances of triggering it by adjusting how you earn and report income. Since many AMT triggers are tied to deductions or specific types of income, planning makes a big difference.

Here are some ways to avoid or lower AMT exposure:

- Time your deductions. For instance, defer paying property taxes or state income tax until the next year if your deductions are already high.

- Exercise incentive stock options cautiously. Large gains from ISOs can create AMT liability, so consider spreading exercises over multiple years.

- Review your investment income. Capital gains count toward AMT income. You might want to hold investments longer or harvest losses to offset gains.

- Use a tax advisor. Professional guidance can help you plan deductions, time income, and use credits effectively.

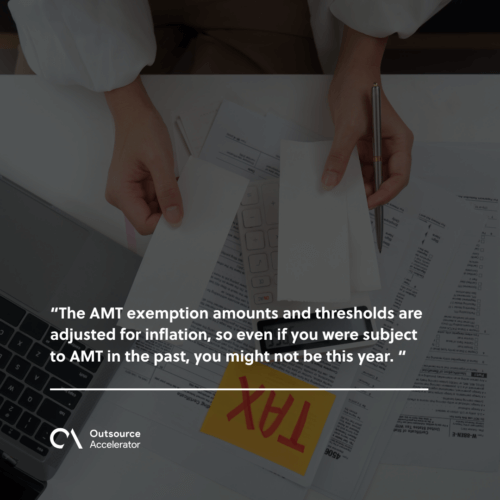

The AMT exemption amounts and thresholds are adjusted for inflation, so even if you were subject to AMT in the past, you might not be this year. Still, it’s wise to check with a calculator or advisor before filing.

Leverage tax preparation and accounting assistance

The AMT is one of those areas where DIY tax filing can be risky if you’re not familiar with the rules. Professional tax preparers and CPAs know how to spot AMT triggers and structure your return to minimize liability.

Dealing with the AMT might feel like one more confusing layer on top of an already confusing system. But it’s manageable once you understand how it works.

Use an AMT tax calculator to get a clear picture of your potential liability, especially if you’re in a higher tax bracket or have a complex financial situation.

If the results surprise you, don’t panic, just plan. A bit of foresight and good advice can keep your tax bill predictable.

Independent

Independent