Top 5 insurance compliance challenges US agencies will face in 2026

This article is a submission by Fusion Business Solution (P) Ltd.-FBSPL. Fusion Business Solution (P) Ltd. (FBSPL) is a Udaipur, India-based company providing Business Process Outsourcing, management, consulting, and IT services, with operations in New York, USA.

Understanding the regulatory pressures, operational risks, and practical strategies US insurance agencies need to manage compliance effectively in 2026.

The regulatory environment for insurance agencies in the United States has become increasingly complex. From evolving state-level rules to stricter consumer protection standards, agencies must navigate a wide range of insurance compliance challenges while maintaining operational efficiency and client trust.

For multi-state agencies, US insurance compliance demands constant monitoring, accurate documentation, and strict regulatory adherence.

Non-compliance can result in penalties, disruptions, and reputational damage. According to Fenergo, global regulatory penalties reached $4.6 billion in 2024, with U.S. regulators driving 95% of enforcement actions.

As regulatory oversight intensifies, agencies must rethink their approach to insurance regulatory compliance. Instead of treating compliance as a reactive obligation, forward-thinking firms are embedding it into their operational strategy.

By adopting structured insurance compliance management, investing in technology, and leveraging insurance agency optimization & consultancy services, agencies can transform compliance from a burden into a competitive advantage.

5 key compliance pressures reshaping insurance agencies

Insurance agencies today face several structural and operational compliance challenges. These issues arise from regulatory complexity, operational inefficiencies, and increased scrutiny from regulators and customers.

1. Multi-state regulatory complexity

One of the biggest insurance agency compliance challenges is the fragmented regulatory framework in the United States. Insurance regulation operates primarily at the state level, meaning each state has its own licensing rules, reporting standards, and consumer protection regulations.

For agencies operating across multiple jurisdictions, this creates a significant compliance burden.

Teams must track license renewals, regulatory changes, and reporting requirements across dozens of states simultaneously. Missing a renewal deadline or misunderstanding state-specific regulations can lead to fines or license suspension.

This regulatory fragmentation makes insurance agency compliance management particularly demanding for growing agencies expanding their geographic reach.

2. Manual compliance processes and human error

Many agencies still rely on spreadsheets, email trails, and manual tracking to manage compliance tasks. These outdated processes increase the risk of human error and missed deadlines.

Manual compliance tracking often leads to:

- Expired licenses or appointments

- Missing documentation during audits

- Incomplete regulatory filings

- Delayed reporting to regulators

Human error in compliance processes can quickly escalate into regulatory violations. Automating insurance compliance management workflows has therefore become essential for agencies seeking to maintain operational accuracy.

3. Documentation and audit requirements

Regulators increasingly expect agencies to maintain detailed documentation of all transactions, policy decisions, and communications.

Incomplete documentation can expose agencies to regulatory scrutiny or Errors & Omissions (E&O) claims. Even minor administrative gaps; such as missing client confirmations or incomplete policy records; can trigger compliance investigations.

This growing emphasis on documentation means agencies must implement strong compliance practices that ensure every policy transaction is properly recorded and auditable.

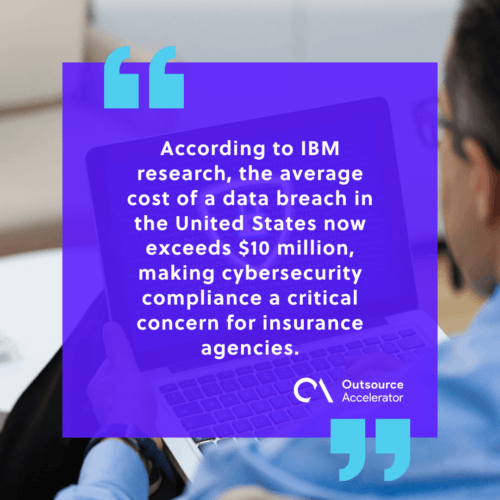

4. Data protection and cybersecurity compliance

Insurance agencies handle large volumes of sensitive personal and financial data. As cyber threats increase, regulators are tightening data protection standards.

According to IBM research, the average cost of a data breach in the United States now exceeds $10 million, making cybersecurity compliance a critical concern for insurance agencies.

Agencies must ensure that their technology systems comply with data protection laws, encryption requirements, and breach notification regulations. Failure to meet these standards can lead to regulatory penalties and reputational damage.

5. AI and digital technology compliance risks

Technology adoption is accelerating across the insurance sector. While AI tools improve operational efficiency, they also introduce new compliance risks.

Automated decision systems used in underwriting, pricing, or claims processing must meet strict regulatory transparency standards. Regulators increasingly require insurers to demonstrate that AI-driven decisions are explainable and free from bias.

If agencies cannot clearly explain automated decisions or demonstrate compliance with regulatory guidelines, they may face investigations or enforcement actions.

Proven strategies to strengthen insurance compliance

Successfully addressing compliance challenges requires more than simply responding to regulatory requirements. Agencies must adopt proactive strategies to improve compliance while integrating compliance management into everyday operations.

1. Implement centralized compliance management systems

A centralized compliance platform allows agencies to track regulatory obligations, licenses, and deadlines from a single dashboard.

Such systems help agencies:

- Monitor state licensing requirements

- Track agent certifications and renewals

- Maintain documentation for audits

- Generate automated compliance alerts

This type of structured insurance compliance management significantly reduces administrative burden and improves regulatory accuracy.

2. Develop standardized compliance workflows

Standardization is critical for maintaining consistent insurance regulatory compliance.

Agencies should establish clearly defined workflows for:

- Policy issuance and renewal

- Documentation and record keeping

- Regulatory reporting

- Complaint management

Standardized processes ensure that every team member follows the same compliance practices, reducing the risk of inconsistent procedures across departments.

3. Invest in continuous compliance training

Compliance responsibilities extend beyond compliance officers. Agents, account managers, and support teams must understand the regulatory environment in which they operate.

Regular training programs help employees stay updated on:

- State regulatory changes

- Licensing requirements

- Ethical sales practices

- Documentation standards

Well-trained teams are less likely to make costly compliance mistakes.

4. Conduct regular internal compliance audits

Proactive internal audits help agencies identify compliance gaps before regulators do.

Internal reviews should focus on:

- License and appointment records

- Documentation completeness

- Customer communication logs

- Regulatory filings

These audits ensure agencies maintain strong insurance agency compliance even as regulations evolve.

The role of licensed account managers in compliance

Licensed account managers play a crucial role in maintaining operational compliance within insurance agencies.

These professionals act as the bridge between clients, carriers, and regulatory frameworks. Their responsibilities often include verifying policy documentation, maintaining accurate records, and ensuring that every transaction aligns with regulatory guidelines.

The role of licensed account managers is particularly important in areas such as:

- Policy servicing and endorsements

- Documentation accuracy

- Customer disclosures and communication

- Compliance monitoring for renewals

Because they work directly with policy data and client information, licensed account managers serve as the first line of defense against compliance errors.

Agencies that invest in well-trained account managers significantly reduce the risk of regulatory violations while improving customer service and operational transparency

Preparing for the future of insurance compliance

Compliance will remain one of the defining operational challenges for insurance agencies in 2026 and beyond. Increasing regulatory complexity, cybersecurity risks, and documentation requirements continue to create significant insurance compliance challenges across the industry.

However, agencies that adopt proactive insurance compliance management strategies can turn these challenges into opportunities.

By implementing structured compliance practices, strengthening the role of licensed account managers, and leveraging insurance agency optimization & consultancy services, agencies can build a robust compliance framework that supports long-term growth.

Ultimately, successful insurance regulatory compliance is not just about avoiding penalties; it is about building trust with regulators, partners, and policyholders.

Agencies that integrate compliance into their operational culture will be better positioned to adapt to regulatory changes and maintain a strong competitive edge in the evolving insurance market.

Independent

Independent