What is Form 8995: A simplified guide to QBI deduction

If you’re a small business owner looking to reduce your tax burden, you may have heard of Form 8995.

But what is Form 8995, and how can it benefit your organization?

This article breaks down everything you need to know about Form 8995 – from its purpose to eligibility requirements. We’ll also explore how it differs from the more complex Form 8995-A, helping you determine which one is right for your situation.

Stay tuned to learn how this form can help you navigate tax savings and streamline your filing process.

What is Form 8995?

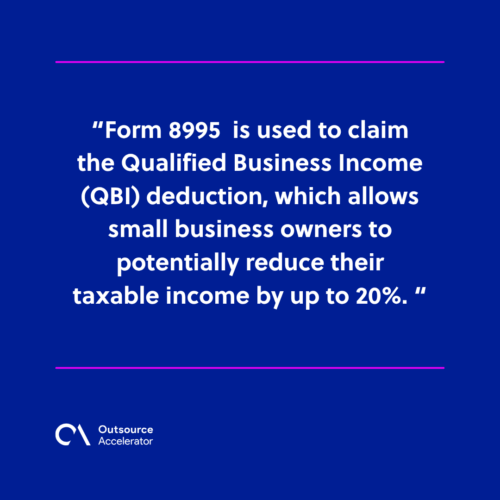

Form 8995 is used to claim the Qualified Business Income (QBI) deduction, which allows small business owners to potentially reduce their taxable income by up to 20%.

It simplifies the process of claiming the QBI deduction, providing a straightforward way to take advantage of this tax benefit. It’s designed for those with simpler tax situations, offering an easier alternative to the more detailed Form 8995-A.

Companies can make the most of their savings without the complexity of additional calculations, making it an essential tool for streamlining tax filing and minimizing tax liability.

Who is qualified to submit Form 8995?

There are several key qualifications to become eligible to submit Form 8995. To qualify for the QBI deduction using Form 8995, a business must be a pass-through entity, particularly:

- Sole proprietorships

- Partnerships

- Limited liability companies (LLCs)

- S corporations

- Estates and trusts

Note: Agricultural or horticultural cooperatives, as well as those with more complex income situations, must use Form 8995-A instead.

Income type qualifications

Only specific types of income can be used on Form 8995 to claim the QBI deduction. These include:

- Pass-through business income

- Qualified REIT dividends (Real Estate Investment Trusts)

- Qualified PTP income or loss (Publicly Traded Partnerships)

- Rental real estate income

Certain income sources, such as capital gains, interest unrelated to business, and foreign income, are excluded from the QBI deduction calculation.

Income thresholds for the QBI deduction

To qualify for the full QBI deduction, business owners must meet the income thresholds. For 2024, the thresholds are:

- $383,900 for married couples filing jointly

- $191,950 for other filing statuses (single, married filing separately, and heads of household)

For 2025, these thresholds increase to $403,200 for married couples filing jointly and $201,600 for all other filing statuses.

If the taxable income exceeds the threshold, additional criteria determine eligibility for a partial deduction. If your taxable income surpasses $485,800 for married filing jointly or $242,900 for other filing statuses, the deduction benefit phases out.

Exclusions from the QBI deduction

Note that certain income types do not qualify for the QBI deduction, including:

- Capital gains or losses

- Interest income unrelated to a business

- Wage income

- Annuities not related to your business

- Income not generated by a U.S.-based firms

- Gains or losses from foreign markets

- Income, loss, or deductions from notional principal contracts

These exclusions must be removed when calculating the deduction.

How to Use Form 8995 for the Pass-Through Deduction

Knowing how to fully leverage Form 8995 for the pass-through deduction can help business owners save significantly on taxes.

Let’s break down how to fill out the form step by step:

Report income and expenses

To begin, report your organization’s income and expenses on Schedule C. Your adjusted gross income should be filed on Form 1040.

You can claim the QBI deduction whether or not you itemize your deductions or take the standard deduction.

Lines 1-4: Business Income and Losses

In Line 1 of Form 8995, list your company name, taxpayer identification number, and each business’s qualified income or loss for the year. Then, on Line 2, total the income or loss from all listed businesses.

If you have a carryover loss from the previous year, include it on Line 3. Line 4 requires you to add the income or loss from Lines 2 and 3. Multiply this total by 0.20 on Line 5 to get 20% of your qualified income.

Lines 6-10: REIT and PTP Income

Next, report any income from Real Estate Investment Trusts (REITs) and Publicly Traded Partnerships (PTPs) in Lines 6 through 10.

Add up this year’s income and any carryover from the previous year, then multiply the sum by 0.20 to get the deduction amount for these income sources.

Lines 11-15: Apply the Income Threshold

For those with income under the QBI threshold (for 2024, $191,950 for single filers and $383,900 for married couples filing jointly), calculate your deduction by comparing two values:

- 20% of your taxable income minus net capital gains

- 20% of your qualified income

Record the lesser value on Line 15.

Lines 16-17: Handle Carryover Losses

If you have a qualified business loss, use Lines 16 and 17 to calculate any carryover to future years.

While you cannot claim a deduction for a negative qualified business income in the current year, you can carry it forward to offset future income.

What is Form 8995: Secure business savings with QBI deduction

Lower your taxable income and retain more of your earnings by carefully following the steps to claim this deduction. Don’t miss out on this opportunity to boost your firm’s financial health!

Independent

Independent